In February 2022, Russia started a full-scale invasion of Ukraine, an event that would shake the global order. The war has already resulted in severe damages to Ukraine – thousands of killed civilians, more than 14 million of people displaced, and over $100 billion in infrastructure damage alone. Yet, the consequences of the war are set to be much more far-reaching, with unprecedented economic consequences for the global community, including rising prices and food shortages.

Recognizing the unlawfulness and global spillovers of the war, governments around the world have punished Russia’s invasion of Ukraine with escalating rounds of sanctions. Individual U.S. states such as California and Illinois pushed to impose additional regulations precluding state pension funds from investing in Russian securities and even mandating divestment. In June 2022, the U.S. Treasury banned U.S. firms from purchasing Russian stocks or bonds on the secondary market. These measures enjoy broad popular support; 85% of Americans favor economic sanctions on Russia, and 75% of Americans support U.S. businesses cutting ties with Russia and ceasing operations (including product sales) in Russia.

Business enterprises, too, are increasingly choosing to disentangle from Russia, even when it is not directly mandated by sanctions. In particular, a growing number of U.S. and European firms have chosen to voluntarily cease or suspend their operations in Russia. In new research, we study the motivating factors behind these decisions. Are these firms’ managers deciding to divest to help Ukraine and punish Russia? Or are they divesting to help their own firms, under pressure from investors? Our results suggest the latter.

We conduct a detailed examination of the relationship between (1) U.S.-traded firms’ decisions to limit their Russian operations and (2) these firms’ stock market returns. There has been an active debate on whether firms exiting Russia benefit or suffer in terms of their stock market valuations. On the one hand, some media outlets report negative effects on operational performance due to declines in earnings, write-downs or write-offs of Russian assets, possible asset seizures, and losses on asset sales due to fire-sale discounts. Others find that financial markets reward firms that exit Russia with positive returns and punish those that stay with negative returns. It is therefore an open question whether reputational damage from staying in Russia outweighs operational risks from leaving, and what the net effect on firms leaving Russia in response to its aggression has been.

We reconcile these seemingly conflicting views and show that the relation between decisions to exit the Russian market and stock price movements of Russia-exposed firms is much more nuanced. For most firms, the decision to exit Russia comes under pressure of prior negative returns: by announcing their exits, firms are able to stop further damage to their valuations.

Specifically, we focus on large firms traded on U.S. stock exchanges that had business operations in the Russian Federation according to their latest public disclosure statements (form 10-K) prior to February 2022. We identify these firms’ exit announcements from current reports (form 8-K), press releases, and media announcements. Over 80% of the firms in the sample have chosen to limit their Russian operations, but there are substantial differences across industries. The healthcare sector is the most likely to retain operations in Russia, with 64% of firms staying, while sectors such as mining and construction are the most likely to withdraw, with less than 6% of firms in these sectors maintaining their operations in Russia. Across the board, larger firms are more likely to exit Russia, potentially due to greater scrutiny and investor attention that these firms face.

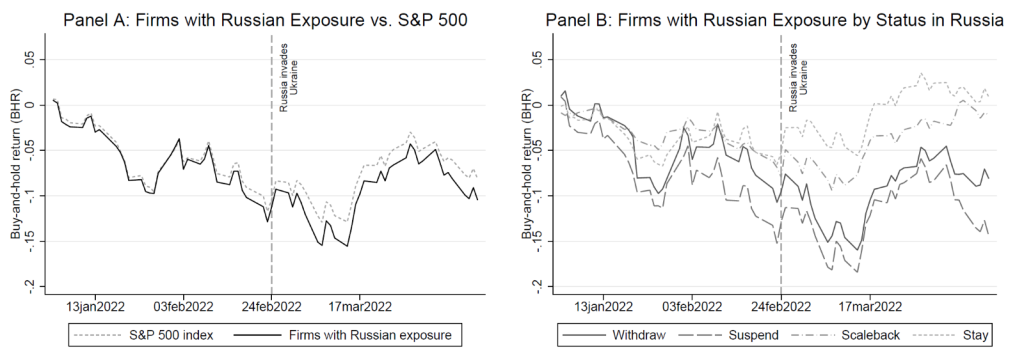

In terms of their stock market performance, U.S. public firms with exposure to Russia began to experience worse performance even before the start of the war, in early February (Figure 1). This likely reflects these firms’ greater risk in anticipation of the war, while Russia amassed troops along the Ukrainian border. Prices of Russia-exposed firms diverged further after the invasion began on February 24, 2022 – and this initial drop was much larger for firms that subsequently ended up limiting their operations in Russia through withdrawals or suspensions. What does this mean? The decision to leave Russia is an endogenous choice for firms with greater risk from Russian exposure, either through direct operational risks or through the risk of reputational damage. In other words, firms left Russia if staying in Russia was costly.

Figure 1. Buy-and-hold returns on U.S. firms by exposure and status in Russia.

This figure shows the evolution of daily buy-and-hold returns (BHRs) on value-weighted indexes of U.S. firms with Russian exposure. Panel A compares firms with Russian exposure to S&P 500. Panel B plots BHRs in value-weighted indexes of U.S. firms with Russian exposure by their status in Russia.

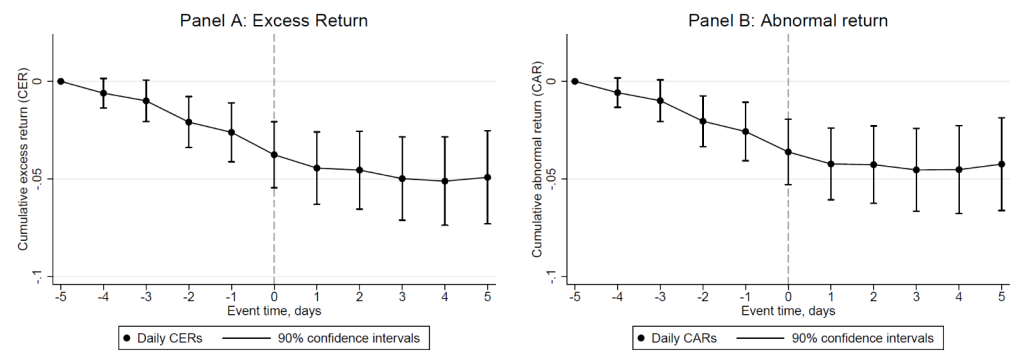

Now, let us take a look at the stock market returns right around firms’ announcements of limiting their Russian operations. In Figure 2, we reproduce the average abnormal stock price reaction from five days before firms announce their exit to five days after. What we see is a strong pre-trend. Prior to announcing a withdrawal or suspension of their operations in Russia, the announcing firms experience a significant negative return: -4% over the course of a single week. However, after the announcement of exit from Russia, this trend immediately stops. This pattern is robust across firms that were more versus less exposed to Russia’s war. Our results support the notion that firms face pressure from their shareholders to discontinue operations in Russia, and exit announcements alleviate this pressure.

Figure 2. Cumulative returns around Russia exit announcement.

This figure shows daily cumulative stock returns on U.S. firms which divested from Russia over the window from −5 to +5 trading days around Russia exit announcement by U.S. firms (Day = 0). Panel A plots cumulative excess returns (CERs) over S&P 500. Panel B plots cumulative abnormal returns (CARs) over S&P 500 estimated using the market model.

We investigate this further by looking directly at the timing of firms’ exit decisions and linking it to firms’ returns. Specifically, we test how a firm’s likelihood of announcing an exit on any given day relates to the recent stock performance of the firm prior to that day. We find that firms’ exit decisions and their timing are strongly related to recent negative stock performance.

Our findings line up with the extensive literature on corporate social responsibility (CSR) and socially responsible investing. Researchers already know that CSR is associated with higher value in firms with higher customer awareness and institutional ownership – it is stakeholders like customers and investors that drive firms to do good. Prior studies provide evidence of widespread behind‐the‐scenes intervention of investors in firm decisions and consider how firms’ investment decisions respond to stock price movements. Our evidence, too, supports the notion that investor attention to firms’ actions can prompt firms to do the ethical thing. Specifically, market pressure from investors compels firms to limit their Russian operations.

So the answer is not as black and white as either firms taking an ethical stance at the expense of profit or experiencing large stock valuation gains as a reward for divestment. Russia-exposed firms suffer losses without exiting – likely due to both operational and reputational risks. The exit decision is a stop-gap measure that doesn’t necessarily bring positive rewards but that does stop the financial losses. Thus, the negative pressure from the firms’ shareholders is an important – and so far largely overlooked – motivating factor for corporate exodus from Russia.

Anastassia Fedyk is an Assistant Professor of Finance at the Haas School of Business of the University of California, Berkeley.

Tetyana Balyuk is an Assistant Professor of Finance at the Goizueta Business School of Emory University.

This post is based on their paper, “Divesting under Pressure: U.S. Firms’ Exit in Response to Russia’s War against Ukraine,” available on SSRN.

The views expressed in this post are those of the authors and do not represent the views of the Global Financial Markets Center or Duke Law.