When addressing the Global Trade in Services Summit in September 2021, President Xi Jinping announced the launch of the Beijing Stock Exchange (BSE), which provides an extra financing channel for the country’s small and medium-sized enterprises (SMEs).[1] The BSE has been built upon the select tier of China’s National Equities Exchange and Quotations (NEEQ), an over-the-counter market for trading shares of public companies that are not eligible for a listing at the more prestigious Shanghai Stock Exchange (SSE) or Shenzhen Stock Exchange (SZSE). Moreover, the BSE has fully implemented China’s latest PRC Securities Law 2020 which led to the biggest overhaul of securities regulation and capital markets law in China in the recent decade, including the introduction of the registration-based Initial Public Offering (IPO) regime.[2] In the first five trading days of the BSE, a batch of 81 SMEs embarked on their IPOs with a total turnover of over 21 billion CNY (around $3 billion), attracting 340,000 qualified investors.[3]

SMEs form the backbone of the Chinese economy. They account for 99% of the total number of enterprises and contribute to over 50% of China’s tax revenue, 60% of gross domestic product (GDP), 70% of technological innovations, and more than 80% of employment.[4] Nevertheless, SMEs have long been facing financing challenges due to the country’s state-dominated banking system that sometimes leads to a less efficient allocation of financial resources.Accordingly, China’s capital markets have gone through a series of reforms to support SME finance since 1990s, such as the foundation of the Securities Trading Automatic Quotation and National Electronic Trading System, the establishment of the Agency Share Transfer System, as well as the rolling out of NEEQ. However, the financing difficulties of Chinese SMEs have not been fully addressed due to the lack of sufficient liquidity in the aforementioned markets. This calls for the further reform of Chinese capital market and the revision of relevant securities laws and regulations to facilitate market growth.

In our recent paper “Beijing Stock Exchange and Multi-Tier Capital Markets: How China Alters Share Listing and Trading Rules to Promote SME Finance?,” we discuss and analyze the functions and special characteristics of BSE and the latest reform of capital markets law in China. The BSE is committed to developing an appealing marketplace for SMEs with inclusive listing thresholds. In line with the listing rules of similar Chinese markets like the Star Market of SSE and the ChiNext board of SZSE, the BSE fully adopts the registration-based IPO regime. Our paper evaluates the BSE’s listing thresholds and IPO rules. Then, it considers the requirements for information disclosure which have been strengthened in light of the latest developments in China’s innovation-driven SMEs. Finally, the paper also assesses the enhanced investor protection and accountability mechanisms in order to foster a more efficient and transparent stock market.

The listing standards of Beijing Stock Exchange

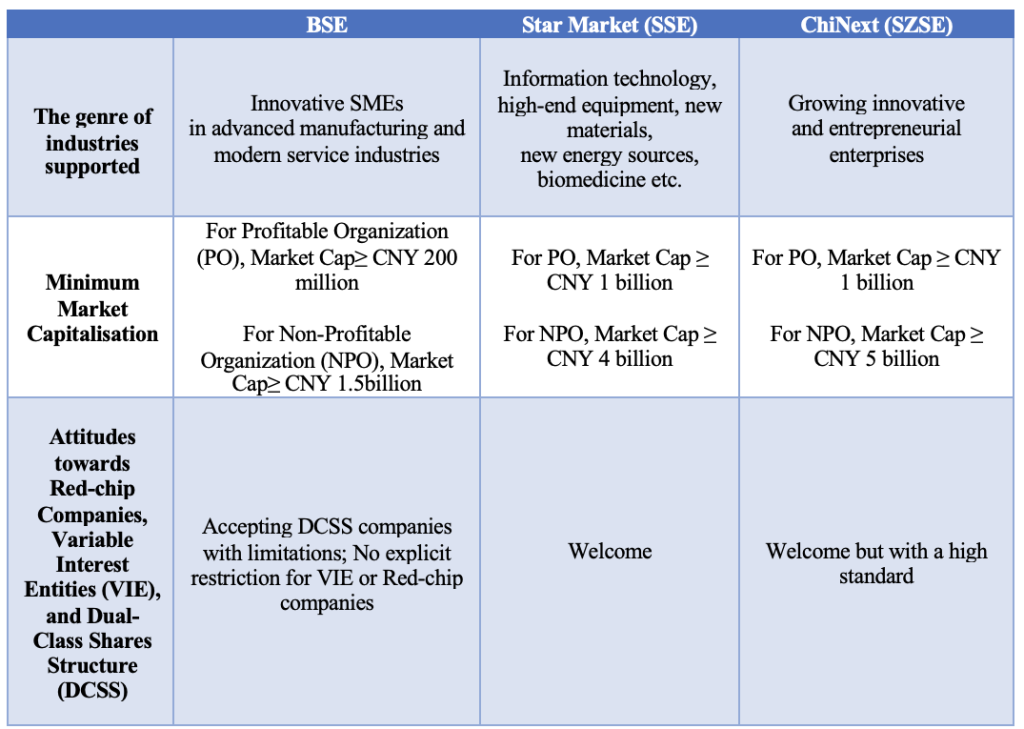

The BSE has introduced a permissive threshold standard under the Listing Rules of Beijing Stock Exchange (Trial), which is primarily modelled on the listing rules of the NEEQ select tier. Companies will be able to obtain a listing if they meet one of the four sets of standards, which mainly focus on the comprehensive assessment of financial indicators together with their innovation ability: (1) Market Cap + Net Profit + Ratio of an Exponentially Weighted Averages (ROEWA); (2) Market Cap + Operating Revenue + Revenue Growth Rate + Cashflow; (3) Market Cap + Operating Revenue + the Proportion of Research and Development (R&D) Investment; or (4) Market Cap + R&D Investment.[5] The required minimum market capitalization is CNY 200 million and CNY 1.5 billion for profitable and non-profitable companies respectively seeking to list shares at BSE, the standard of which is much lower than that of Star Market and ChiNext considering SMEs’ special features. Government support, such as financial subsidies covering part of IPO expense, will be available for SMEs to provide financial assistance for their floatation. In addition, the companies adopting dual-class shares structure (DCSS) are also welcomed by the BSE, and there is no restriction on red-chip companies and variable interest entities (VIE), showing BSE’s open attitude towards SMEs that adopt innovative corporate finance strategy and governance structure.

The registration-based IPO system and information disclosure requirements

For a long time, China’s stock markets have been employing a so-called approval-based IPO system under which listing companies would need to be extra censored and approved by the securities regulator. Despite BSE being founded on the NEEQ’s select tier, it has completely embraced the new registration-based IPO regime as a more market-oriented and cost-effective listing procedure, which is based on adequate information disclosure rather than substantial regulatory scrutiny. In terms of the prospectus regime, the validity period of financial statements has been extended by two months compared with 6+1 months for the select tier, which is consistent with the period rules held by the Star Market and ChiNext.[6] Furthermore, the new Listing Rule of BSE has made a more streamlined and speedy process for the listing entities, as the time for reviewing the application documents has been shorted to 2 months.[7] Thus, it only takes approximately 6-8 months for a company meeting the formalities and pre-set standards of the BSE to float their shares.The enhanced information disclosure is to address the information asymmetry between corporate issuers and their investors. Most rules of BSE are in line with the information disclosure regime under PRC Securities Law 2020, similar to that implemented for the select tier and other segments of SSE and SZSE. For instance, issuers must ensure the authenticity, integrity, and precision of the information disclosed and they are also responsible for disclosing critical incidents and explaining relevant causes and subsequent consequences.[8] Nonetheless, some rules pertinent to material changes of the performance projection system, the transactions and substantial matters etc., have been modified to accommodate the interests of SMEs.

The investor suitability and accountability mechanisms

The specter of fraud will never disappear if the regulatory regime is solely based on mandatory information disclosure. To foster an active, transparent, and efficient capital market of high integrity, the BSE gives it its best shot by instituting dual safeguard mechanisms: first, it strives to comply with the “Rules of Investor Suitability,” and second, it seeks to establish a sound accountability mechanism. To entice more investors to trade in the venue, thereby increasing capital amounts and liquidity in the nascent market, a more relaxing daily price fluctuation has been introduced on BSE, which is as much as 30% – compared with the 20% limit for Star Market and ChiNext and 10% for the mainboards of SSE and SZSE.[9]Besides, the requirements for the eligible retail investors on BSE are the same as those regulated in the two segments, that is: two years of trading experience and more than CNY 0.5 million financial assets holding for at least 20 trading days.[10]

Moreover, a sound accountability mechanism contributes to market fairness and integrity. Apart from the rigorous penalties, such as a fine of up to 100% of the raised fund for financial fraud regulated in PRC Securities Law, for corporate issuers who violate rules less severely, the BSE has introduced self-regulated flexible measures, like criticizing in a circulated notice, publicly denouncing, and making corrections within a time limit etc. Moreover, China’s State Council has issued a decree to enact new rules, which came into force in January 2022, stating that corporations that violate securities laws but are likely to rectify illegal behaviors to eliminate adverse effects or compensate investors for losses will have their investigation terminated if it is approved by the securities regulator.[11] Obviously, all the above rules have been made to safeguard the investor interests by considering the special characteristics of SMEs, which is able to create a forward-looking and sound capital market legal regime.

Looking ahead

The high-profile launch of the BSE, coupled with the promulgation of targeted rules for SME finance, indicates that the Chinese government is determined to address the financing challenges confronted by SMEs. It adheres to the preeminent rules used by the NEEQ select tier, ChiNext, and the Star Market, with certain adjustments to suit the practical needs of SME issuers. Furthermore, with a cross-market transferring mechanism being established, the BSE-listed SMEs will have the opportunity to directly float their shares at SSE or SZSE once they grow bigger in size. With favorable policy support, the BSE is likely to play an important role in Chinese capital markets which complements the more established SSE and SZSE. So far, mainland China has got three major stock exchanges located in the country’s north (BSE), middle (SSE), and south (SZSE), as they together form an institutionally sound, multi-tier, and interconnected capital market financing system in the world’s second largest economy.

Lerong Lu is a Senior Lecturer at the Dickson Poon School of Law, King’s College London

Jiujing Ye is an Attorney-at-Law in China

This post is adapted from their paper, “Beijing Stock Exchange and Multi-Tier Capital Markets: How China Alters Share Listing and Trading Rules to Promote SME Finance?” available on SSRN.

The views expressed in this post are those of the authors and do not represent the views of the Global Financial Markets Center or Duke Law.

[1]James T. Areddy, “China to Launch Beijing Stock Exchange to Steer Investment Into Innovation”, Wall Street Journal (2 September 2021), available at https://www.wsj.com/articles/china-to-launch-beijing-stock-exchange-to-steer-investment-into-innovation-11630622825.

[2] Lerong Lu, “Reforming corporate share-listing rules in China: understanding the rationale and advantages of the registration-based IPO regime” (2021) 42 Company Lawyer 236.

[3]Global Times, “1st trading week of Beijing Stock Exchange meets expectations with 340,000 new investors coming online” (21 November 2021), available athttps://www.globaltimes.cn/page/202111/1239536.shtml.

[4] Chinese Government, “We will give policy support to small and medium-sized enterprises” (1 April 2021), available at http://www.gov.cn/zhengce/2020-04/01/content_5497938.htm.

[5] Listing Rules of Beijing Stock Exchange 2021 (Trial), Section 2.1.3.

[6] Rules for Review Offering Shares to Non-Specific Qualified Investors of Beijing Stock Exchange 2021 (Trial), Article 43.

[7] Rules for Review Offering Shares to Non-Specific Qualified Investors of Beijing Stock Exchange 2021 (Trial), Article 38.

[8] Listing Rules of Beijing Stock Exchange 2021 (Trial), Section 5.3.2.

[9] Trading Rules of Beijing Stock Exchange 2021(Trial), Section 3.3.11.

[10]Rules of Investors Suitability of Beijing Stock Exchange 2021 (Trial), Article 5.

[11] Xinhua, “China unveils regulation on securities, futures violations” (30 November 2021), available at http://en.people.cn/n3/2021/1130/c90000-9926128.html.