Climate change poses significant risks to the private sector, which researchers estimate to be in the order of $2.5-24 trillion, or up to 17% of global assets under management. However, given the most significant climate change risks may not materialize within the tenure of current corporate and financial actors, direct incentives to avert the tragedy of the horizon may be inadequate. In this vein, there is a clear and crucial need for design and evaluation of incentive mechanisms to enable adaptation through behavioral change and the promotion of collective action.

Given the preeminent view of executive compensation among academic, policy, and practitioner circles as a means of directing corporate behavior, it is unsurprising that managerial pay awards are being tied to climate targets. For instance, awarding higher bonuses to managers achieving better carbon performance through reduction of carbon emissions. However, a key concern is that, even if effective, shareholders may reject linking managers’ pay to carbon performance if it results in diminution of near-term financial returns.

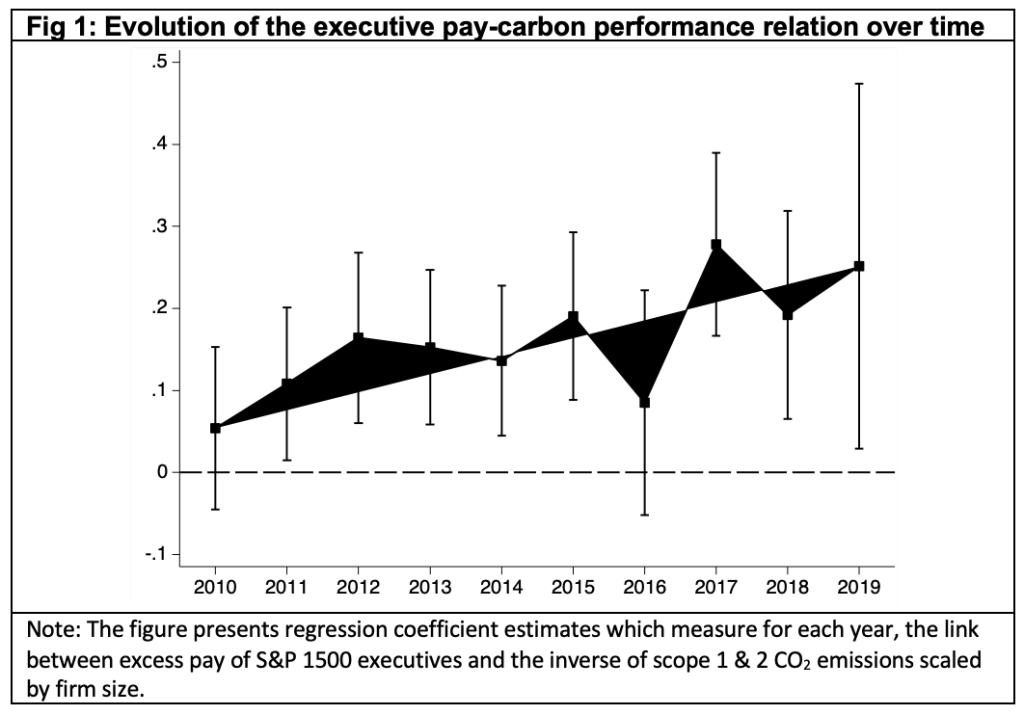

Despite a paucity of companies to date setting explicit climate-related pay targets, in our recent study, we find that a significant relation between compensation pay-outs and carbon performance has nevertheless developed among S&P 1500 companies over recent years. The financial incentives for managers to drive reductions in CO2 emissions of their companies appear to have existed for some time and are getting stronger (Fig 1). Controlling for other factors, such as company size, financial performance (e.g., TSR), tenure, and industry, companies with lower scope 1 and 2 emissions are able to award more generous pay-outs to executives, on average.

In further tests, we find the carbon-pay relation to be stronger among companies with higher levels of institutional shareholdings and/or higher stock liquidity, both of which have been shown to be associated with more effective monitoring by financial institutions; the latter, for example, facilitates credible exit threats. On the other hand, we find that shareholders, more broadly, do not appear to factor in carbon performance when voting on proposed executive compensation in say-on-pay resolutions. Below, we put these seemingly contradictory empirical results into context.

Institutional scrutiny along the path to net-zero

One explanation for our findings is that low-carbon firms now face relatively reduced levels of adverse scrutiny, particularly from institutional investors and the media, and that this has made it relatively easier for managers at those firms to extract rents. As Environmental, Social, and Governance (ESG) issues – particularly those related to climate impact – now garner mainstream attention, carbon track record has become a core criterion by which companies and their managers are evaluated publicly. Research shows that public acclaim can increase managers’ ability to extract rents through higher compensation awards, even if they do not deliver higher financial returns.

Considering the role of institutional investor monitoring, evidence points towards an emerging consensus among institutional investors that climate risk has financial implications for their portfolios, and moreover that they consider risk management and engagement with firms to be a better approach to addressing climate risks than divestment. In addition, institutional investors may act to reduce carbon emissions of portfolio firms due to altruism, social pressure, or to improve their image, e.g., to attract clients. Recent research finds that, as a result, the “Big Three” investors (Blackrock, Vanguard, and State Street Global Advisors) have increasingly focused their engagement efforts on firms with higher carbon emissions.

Our study contributes by revealing that increased attention on, and discourse around, climate impact not only places a direct pressure on companies to do good, but it also indirectly creates financial incentives for managers to curb carbon emissions at the companies they operate. To the extent that companies with high CO2 emissions come under increasingly heavy scrutiny, they are less able than low-carbon counterparts to legitimize high pay awards.

Why shareholder votes on climate may fail

Significant plans are afoot to encourage or mandate companies to put climate action plans to a vote of shareholders, in so-called say-on-climate resolutions. Proponents argue that say-on-climate votes will enable shareholders to hold companies to account on their climate change strategies and improve oversight of companies’ plans to achieve ambitious net-zero targets. However, acceleration of corporate carbon reductions through say-on-climate is predicated on the idea that investors value ambitious climate change abatement above preservation of short-term financial interests, and to a greater extent than managers.

A reason why they might value ambitious climate change abatement is if shareholders take a longer-term perspective than managers, and more readily acknowledge the severity of the long-term financial risks associated with climate change. The benefits of carbon reduction, through reduced climate risk, may accrue mostly beyond the tenure of current corporate actors. However, despite the attitudes of some investors towards climate risk changing, it remains unclear whether investors at large would vote for more ambitious carbon abatement.

While some institutional investors may herald the longer-term view, other investors display copious short-termism, pursuing short-term returns and dividends while neglecting long-run fundamentals. Some investors may also underestimate the implications of climate risk on firm fundamentals for reasons including incomplete information and behavioral biases, e.g., “local thinking.” Because catastrophic climate change is unprecedented, and the implications are just beginning to materialize, information about its severity for cash-flows may be ignored. Indeed, experts across the academic, private, and public sectors overwhelmingly agree that financial markets do not, at present, sufficiently price in climate risks.

There is a clear need for more research to evaluate whether say-on-climate votes could be effective in accelerating climate action, however, conclusions from such research may not be drawn for some time. In the meantime, we may be able to draw some insight from research examining shareholder votes on other resolutions, e.g., advisory say-on-pay votes. Prior research on say-on-pay votes suggest they are used as a mechanism to better align managers with shareholders’ economic interests. We argue that if shareholders also wish managers to reduce carbon emissions, they will tend to vote more favorably for those that do in the say-on-pay.

To the contrary, we find no evidence in our study that shareholders dissent less against proposed executive compensation in the say-on-pay when firms display better carbon performance. This suggests that shareholders, at large, view pay-for-carbon-performance as an agency cost, and arguably also reflects general antipathy by investors towards costly carbon reduction. This suggests that, unless broader investor attitudes change, shareholder votes on climate strategy may not be the panacea expected. If say-on-climate does anything, it may be to legitimize inaction, to promote cost effectiveness, to neuter, or to delay, rather than to drive forward ambitious and necessary corporate carbon reduction.

Danial Hemmings is a Lecturer in Finance at Bangor Business School at Bangor University.

Lynn Hodgkinson is a Professor in Accounting and Finance at Bangor Business School at Bangor University.

Gwion Williams is a Lecturer in Finance at Bangor Business School at Bangor University.

This post is adapted from their paper, “A ‘green light’ for executive pay? Shareholder monitoring and pay-for-carbon-performance” available on SSRN.

The views expressed in this post are those of the authors and do not represent the views of the Global Financial Markets Center or Duke Law.

This is a tough one. Near term, executives and shareholders are reluctant to make those investments because the short-term effect is a dilution to earnings. And in Business the overriding focus is on increasing shareholder value at all cost. This mind set has to change a bit and companies have to have a long-term strategy regarding climate change. Executives should have a portion of their compensation linked to lowering their areas overall carbon footprint.