Last September, The Economist published an article titled “Why Covid-19 will make killing off zombie firms harder.” The article fueled an already widely debated topic and expresses general concerns that schemes put in place to help pandemic-stricken businesses to survive might exacerbate therise of the corporate undead.

The ongoing crisis highlights the necessity of analyzing the ”zombification” phenomenon; a constellation in which public support schemes and bank lending activities could keep non-viable firms afloat for longer. There are several examples of well-known public companies that have been in dire straits since the Global Financial Crisis and would have not been able to survive without financial assistance. Similarly, with the Covid-19 pandemic, aseries of government measures implemented to support European businesses might have allowed companies that would have otherwise filed for bankruptcy to continue their activities. Existing studies refer to these occurrences as zombie companies, i.e., business entities that are unable to cover debt service costs over an extended period of time. Their negative impact on productivity and growth has been documented in several studies. Plotting zombie shares worldwide, it becomes clear that the zombie phenomenon has been a first-order issue since the Global Financial Crisis.

Figure 1: Zombie Trend in Europe and in the Rest of the World. This figure plots the share of zombie companies in Europe (32 countries considered) to the right and in the Rest of the World to the left. The Rest of the World includes Asia and Latin America and excludes the United States andCanada. The plotted timeframe of analysis considers the years from 1996 to 2018. We measure zombie companies following Banerjee and Hofmann (2020).Source: De Martiis, Heil, Peter (2021) on Compustat Global data.

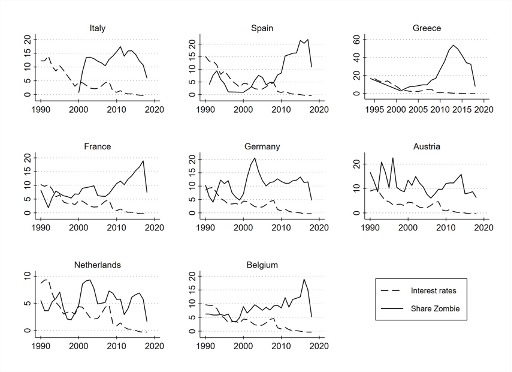

Focusing on eight European countries, we document an increase in the share of zombie firms following economic downturns, particularly after the Global Financial Crisis. Several peaks are registered over a period of time that saw interest rates close to zero and the announcement of monetary policy measures aimed at reviving the corporate sector. This motivates the highly debated question, are zombie companies an unintended consequence of relaxed monetary policy?

Figure 2: Zombie Shares and Short-Term Interest Rates. This graph plots the share of zombie companies, black line, and the short-term interest rates, black dashed line, in eight European countries from 1990 to 2018. We measure zombie companies following Banerjee and Hofmann (2020). Source: DeMartiis and Peter (2021) using Compustat Global and OECD data.

Using the Compustat Global Fundamentals database, a comprehensive market and corporate financial database, we examine the association between monetary policy and non-viable firms’ status on a firm level-basis. The goal is to understand to what extent the low interest rate environment can affect the status of zombie companies directly, or through its impact on the state of the economy. Theoretically, if interest rates are low for long, allcompanies should benefit, viable and non-viable, as they would have the incentive to carry on their planned investments.

The accommodative monetary policy measures adopted by the European Central Bank in response to the crisis period helped support productivity by easing credit conditions for non-financial companies, as well as households, with the aim to support viable, but vulnerable, firms. It remainsunclear whether these measures can increase the misallocation of capital across firms, i.e., whether zombie companies have benefited from such non-conventional monetary measures. Facilitated access to credit for unprofitable and potentially unproductive zombie firms, however, wouldfurther depress economic growth, counteracting goals of unconventional monetary policy.

It has been shown that monetary easing fosters growth in more credit-constrained environments. Nonetheless, given the existence of financial frictions, only viable firms would react to the incentives and increase capital stock, while non-viable firms would be less responsive.

To shed light on the above mechanism, we examine the link between short-term interest rates, a proxy measure of monetary policy, and non-viable firms’ status. Based on estimations of Panel Logit models, we find a negative and significant effect of short-term interest rates on the likelihood of zombie status, supporting the argument that low interest rates for long can constitute a favorable environment for zombie firms’ livelihood—in agreement with Banerjee and Hofmann (2018). This finding is not confirmed to the entire class of distressed firms, a result that can be explained by the unique features of zombie companies. In addition, we employ a difference-in-differences design and test the reaction of non-viable firms to a specific policy – the ECB’s Corporate Sector Purchase Program – a non-conventional monetary program aimed at easing firms’ financing conditions. Our results show no evidence of misallocation of credit within this program, suggesting that credit constrained firms are not responding to the lowborrowing costs offered by the Corporate Sector Purchase Program. To derive a broader picture of the impact of monetary policy on non-viable firms, we not only consider zombie firms, but repeat our analyses for distressed firms as well.

Considering that corporate default decisions can depend on monetary policy through its impact on expected inflation, we study the effect of inflation on zombie and distressed firms. In agreement with Bhamra, Fisher and Kuehn (2011), our results show that an increase in inflation can lead to adecrease in non-viable firms’ status.

Since the implementation of monetary policy measures coincidences with recession periods, we augment our analysis by examining two businesscycle indicators, GDP growth, and the Composite Leading Indicator, to examine their impact on the status of non-viable firms. The CompositeLeading Indicator anticipates turning points six to nine months before they occur and is composed of economic indicators capturing orders and inventory changes, financial market and business confidence information, and key sectors and trends for small open economies. We complement thisexercise with an analysis of recession events, the Dot-com Bubble, the Global Financial Crisis, and the European Debt Crisis, to understand theirdistinctive effects on non-viable firms. Accounting for indirect effects of monetary policy via the business cycle, we find that expected turning points, measured by the fluctuation of economic activity around its long-term trend, increase zombie prevalence. The recession events further suggest thatthe probability of zombie status is affected by economic downturns. Consequently, if the number of companies undergoing zombification increases with business cycle downturns, economies might struggle with the consequences of increasing zombie shares in addition to the Covid-19 inducedeconomic burdens.

Among the main firm-specific features, we find—in line with those of Japanese zombie firms—that zombies are smaller in size, with lower profitability, and long-term debts and liabilities. Comparing the characteristics of zombie firms with that of distressed firms, our results indicate that profit margin—a predictor of future profitability—is decisive in categorizing zombies, but not distressed firms. At the same time, distressed companies appearlarger, while leverage is a predictor of both types of firms.

Altogether, our research validates the argument that low interest rates can be a breeding ground for zombie firms. However, monetary policy is not theonly factor explaining the high incidence of zombie shares across European countries. Poor economic conditions increase the likelihood of non-viable firms and turning points in economic activity signal a rise in zombie prevalence. Given the strong dependencies of non-viable firms on the state of the economy, an indirect effect of low interest rates on the business cycle should be considered when examining the phenomenon of zombie companies.Our results provide new evidence on the existence of offsetting channels explaining zombie prevalence and highlight the importance of distinguishing zombies from non-zombies and other types of unviable firms, and to closely monitor the dynamics of zombie companies during andafter crisis periods.

Angela De Martiis is Finance Postdoctoral Researcher at the University of Bern, Institute for Financial Management

Franziska J. Peter is Professor of Empirical Finance and Econometrics at the Zeppelin University

This post is adapted from their paper, “When Companies Don’t Die: Analyzing Zombie and Dis- tressed Firms in a Low Interest Rate Environment”available on SSRN.

Yes, the environment has been changed after COVID 19 situation.

Companies should have to be more careful and do in-depth analysis of the market.

Yes, completely agree