When Tim Cook replaced Steve Jobs as CEO of Apple in 2011, the company’s employees — along with shareholders and the rest of the world — wondered if he could fill his larger-than-life predecessor’s shoes and maintain the company’s momentum. While the business press continues to pay attention to CEOs having the pressure to catch up with the heightened firm performance left behind by a rising star, there is a dearth of large-sample evidence about this “big shoes to fill” phenomenon and the underlying mechanism remains poorly understood.

In our recent study, “Big Shoes to Fill: CEO Turnover and Pre-Appointment Firm Performance,” we hypothesize that variation in firm performance prior to a CEO’s appointment influences the evaluation of a CEO during his or her tenure. In other words, corporate boards benchmark CEO performance not only against peers but also against the company’s historical performance.

Summary of Main Findings

Using a quarter-century sample from 1993 to 2017 of CEO turnover among Standard and Poor’s 1500 firms, we estimate a model of the probability of CEO dismissal, where low firm performance (e.g., negative returns) is the main determinant of getting fired. In this model, the magnitude of a (negative) coefficient on firm performance indicates the relative sensitivity of CEO dismissal to underperformance. In addition, we show that the (negative) coefficient also varies with firm performance under the prior CEO. This analysis intends to capture whether the “patience” of a board, when deciding whether to fire a CEO, depends on the prior CEO’s success or failure.

We demonstrate that as pre-appointment firm performance increases, the CEO turnover-performance sensitivity coefficient decreases. This negative coefficient suggests that an underperforming CEO is more likely to be dismissed for performance if appointed at a firm with superior past performance (see Figure 1). The effect is sizable — an increase in pre-appointment firm performance from the 10th to the 90th percentile triples the sensitivity of CEO turnover to firm performance.

Figure 1: Effect of Pre-Appointment Firm Performance on CEO Turnover-Performance Sensitivity

A Theoretical Model of the “Big Shoes to Fill” Effect

We use a relatively simple theoretical Bayesian learning model that describes how CEO dismissal decisions are affected by pre-appointment firm performance. The standard CEO turnover model suggests that owners learn about their CEO’s ability from realized firm performance and dismiss their CEO if performance falls below their expectations. We extend the standard CEO turnover model and posit that historical firm performance not only reflects a prior CEO’s ability, but also reveals information about firm-specific fundamental values that persist over time. These fundamental values are related to factors such as unique physical assets, human capital, systems and processes, products and services, competitive strategies, and market opportunities. Upon observing firm performance prior to a CEO’s appointment, owners thus use the Bayes’ theorem to learn about the quality of their firm’s fundamentals and recalibrate their beliefs about future firm performance. Bayesian learning, as a popular tool in probability theory and statistics, allows corporate owners to update their beliefs about firm quality accurately based on the observed past firm performance signals.

For instance, superior pre-appointment performance increases owners’ beliefs about firm asset quality, thereby increasing their performance expectations for their new CEO. Consequently, higher expectations lead to a greater likelihood that an underperforming CEO will be dismissed when succeeding a high-performing CEO relative to one with similar performance but following a low-performing CEO. Specifically, the sensitivity of CEO turnover to firm performance increases in pre-appointment firm performance.

Additional Evidence Supporting the Bayesian Learning Model

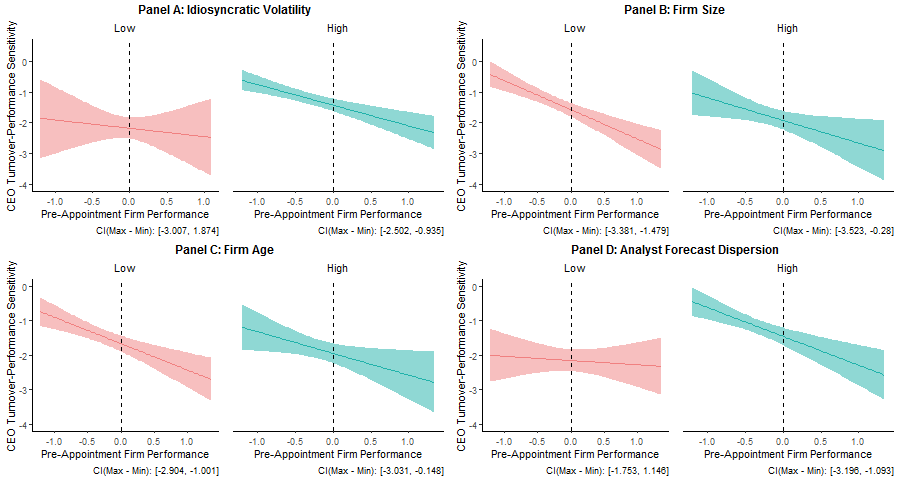

We conduct two additional analyses to explore the Bayesian learning mechanism’s implications. First, our framework suggests that belief revisions in light of historical firm performance increase with uncertainty about firm fundamentals. Consequently, we expect that the effect of pre-appointment firm performance on CEO performance-turnover sensitivity increases in firm uncertainty. We examine how our documented relation varies with firm uncertainty by estimating our model within firm subsamples partitioned by their idiosyncratic volatility, firm size, firm age, and analyst forecast dispersion. Consistent with our prediction, we find that the effect of pre-appointment firm performance on CEO performance turnover likelihood is more pronounced in firms with relatively greater fundamental uncertainty (See Figure 2).

Figure 2: Effect of Uncertainty about Firm Fundamentals

Second, the Bayesian learning model implies that the weight placed on previously observed signals declines over time as newer information accumulates. Therefore, we expect that pre-appointment firm performance becomes less informative over a CEO’s tenure as more information about their ability accumulates. Consistent with this, we find that the effect of pre-appointment firm performance on CEO turnover-performance sensitivity declines monotonically over a CEO’s tenure.

Alternative Explanations to the “Big Shoes to Fill” Effect

While our results collectively support the Bayesian learning mechanism (i.e., a rational story for our results), we discuss two potential alternative explanations for our main finding.

One concern is that our results are driven by a “contrast effects” bias rather than by Bayesian learning. This bias implies that owners form biased expectations of CEO ability by contrasting it to their predecessor’s competence. For example, owners mistakenly perceived their CEOs as less able than they actually are when they succeed a “superstar” CEO; thus, they are likely to be dismissed.

Another concern is that our main result is attributable to variation in a firm’s corporate governance quality. It is possible that boards at poorly performing firms are less engaged, or are inferior learners about CEO ability, than those at well-performing firms, thus allowing untalented CEOs to retain their appointment longer than merited. However, our empirical evidence does not support these alternative explanations.

Our Conclusion and Contribution

Overall, our results suggest that CEOs are not only held accountable for firm performance under their own management but that owners’ evaluations of their CEOs are also influenced by pre-appointment firm performance. More broadly, our findings suggest that learning about a firm’s fundamental value, embedded in historical performance, is consequential for CEO dismissal decisions.

Our paper furthers our understanding of CEO dismissal decisions by highlighting that turnover is not only related to firm performance under an incumbent’s direction but also affected by the performance before he assumes office. Additionally, while the relative performance evaluation (RPE) literature largely focuses on the relative assessment of CEO quality to contemporaneous peers, our paper extends this inquiry by showing that corporate owners form performance expectations for their executives based on their predecessor’s performance. Finally, our work draws on the literature that explains aspects of management incentives and governance decisions using the learning process about management ability.

References

Jensen, M.C. and Murphy, K.J., 1990. Performance pay and top-management incentives. Journal of Political Economy, 98(2), pp.225-264.

Gibbons, R. and Murphy, K.J., 1990. Relative performance evaluation for chief executive officers. Industrial and Labor Relations Review, 43(3), pp.30-S.

About the Authors

Miguel Minutti-Meza is a Department Chair and an Associate Professor of Accounting at the Miami Herbert Business School.

Dhananjay Nanda is Vice-Dean of Faculty & Research and Professor of Accounting at the Miami Herbert Business School.

Rosy Xu is a PhD candidate in accounting at the Miami Herbert Business School.

This post is adapted from their paper, “Big Shoes to Fill: CEO Turnover and Pre-Appointment Firm Performance,” available on SSRN.